SMM, January 3:

In 2024, the supply gap for bauxite remains unchanged. Domestic alumina production exceeds expectations, with the increase in bauxite supply unable to meet the growth in demand. The bauxite supply gap expands compared to 2023. Coupled with sustained significant profitability in alumina, alumina refineries show increased acceptance of high-priced bauxite, boosting bauxite prices upward.

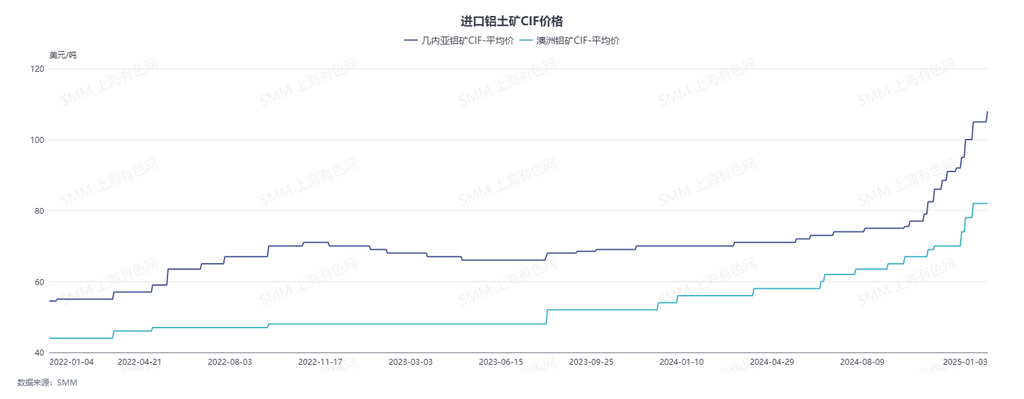

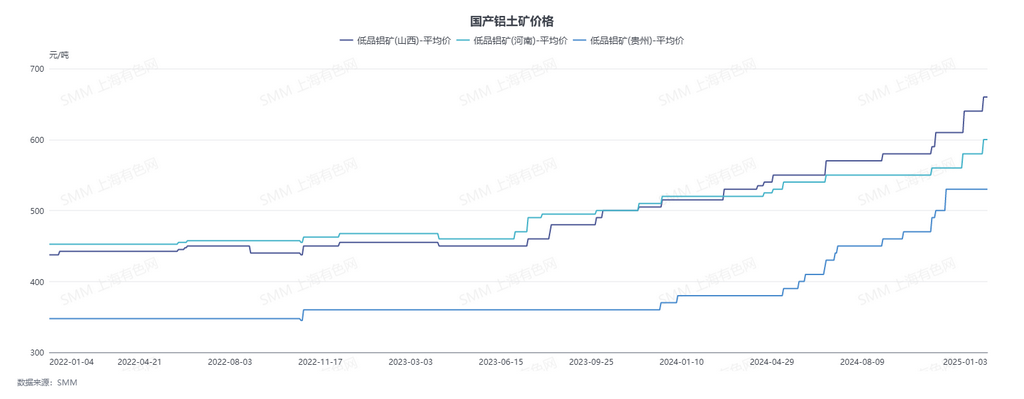

As of December 31, 2024, CIF prices for Guinean bauxite stood at $105/mt, up 50% from $70/mt at the beginning of the year; CIF prices for Australian bauxite were $82/mt, up 51.9% from $54/mt at the beginning of the year. The self pick-up price for low-grade bauxite in Shanxi, excluding VAT, was 660 yuan/mt, up 145 yuan/mt (28.2%) from 515 yuan/mt at the beginning of the year. In Henan, the self pick-up price for low-grade bauxite, excluding VAT, was 660 yuan/mt, up 140 yuan/mt (26.9%) from 520 yuan/mt at the beginning of the year. In Guizhou, the self pick-up price for low-grade bauxite, excluding VAT, was 530 yuan/mt, up 160 yuan/mt (43.2%) from 370 yuan/mt at the beginning of the year.

Alumina imports decreased, while domestic bauxite supply constraints limited alumina production increases, causing alumina prices to surge significantly.

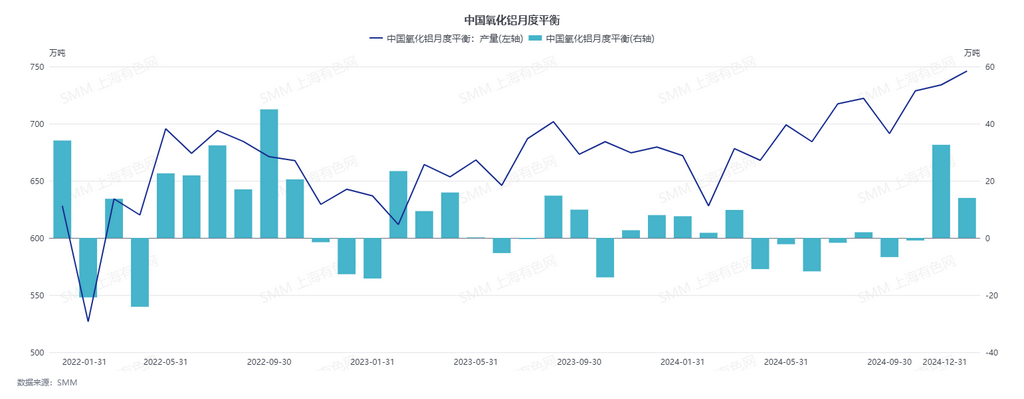

Starting from Q2 2024, overseas alumina supply decreased, leading to a sharp price increase and the closure of the import window. China gradually shifted from being a net importer to a net exporter of alumina. From January to November 2024, China recorded a net export of approximately 193,000 mt of alumina, compared to a net import of 425,000 mt during the same period in 2023. In Q2 2024, reduced imported alumina supply and increased alumina demand due to the resumption of aluminum production in Yunnan turned the domestic alumina market into a supply deficit, driving the first significant price surge for alumina.

Approaching Q4 2024, the market anticipates that the supply-demand imbalance for alumina will re-emerge. On the supply side, the alumina import window remains closed, and domestic alumina refineries face production constraints due to limited ore supply. Additionally, the market expects that alumina calcination may be restricted during the heating season. On the demand side, the market anticipates that aluminum smelters will stockpile alumina for the winter, while the risk of aluminum production cuts in Yunnan decreases. In Q3, the domestic alumina market remained tightly balanced. Coupled with market expectations of a supply-demand imbalance in Q4, spot alumina prices experienced a second significant surge.

The surge in alumina prices and profits stimulated production, increasing bauxite demand.

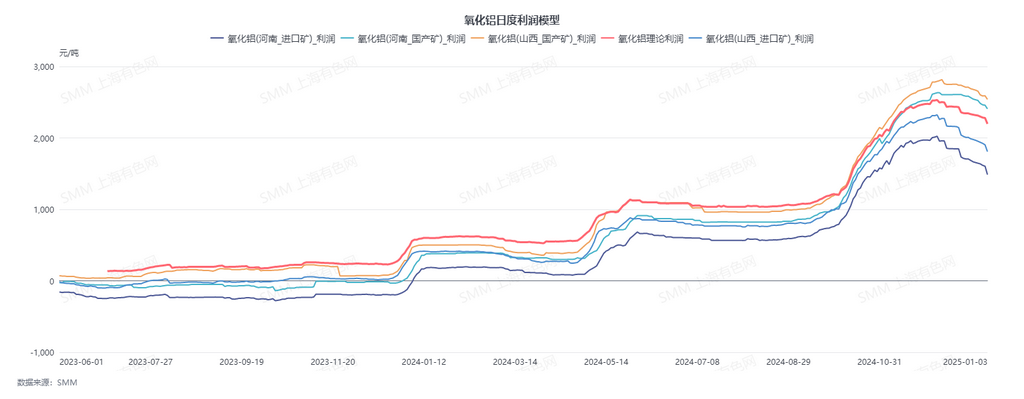

After the first significant price surge, the average profit in the alumina industry expanded to 1,000-1,100 yuan/mt. Following the second surge, the average profit reached nearly 2,500 yuan/mt. Stimulated by high profitability, domestic operating capacity for alumina showed an increasing trend, with total production exceeding initial expectations. From January to December 2024, total alumina production reached 83.69 million mt, up 4.86% YoY, thereby increasing demand for bauxite.

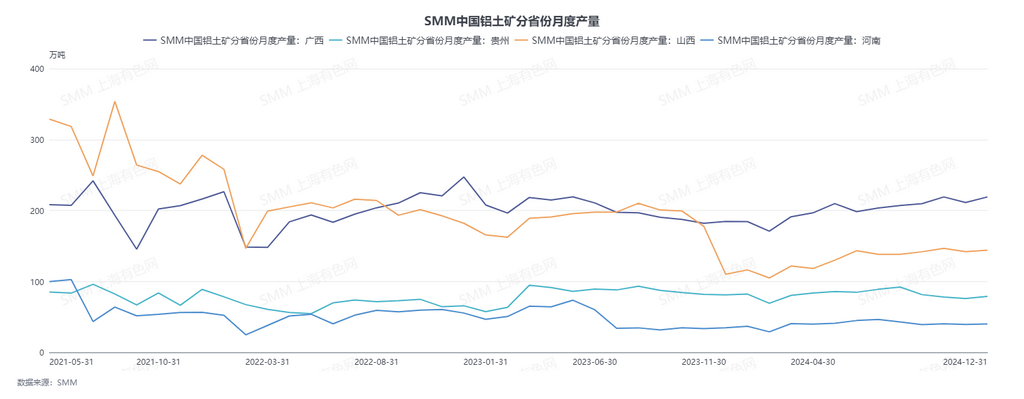

Bauxite production in Shanxi and Henan failed to resume, reducing domestic bauxite supply.

Since July 2023, bauxite production in Sanmenxia, Henan, has been suspended. From late November to early December 2023, large-scale production halts occurred in Lvliang, Shanxi. Starting from May to June 2024, some suspended bauxite mines in Shanxi and Henan resumed production, but the recovery was minimal, leading to a significant decline in bauxite production in these regions. From January to December 2024, bauxite production in Shanxi totaled 15.86 million mt, down 27.8% YoY, while Henan's production totaled 4.81 million mt, down 14.7% YoY. The production cuts in Shanxi and Henan reduced domestic bauxite supply, with total domestic metallurgical bauxite production amounting to 58.08 million mt, down 11.3% YoY.

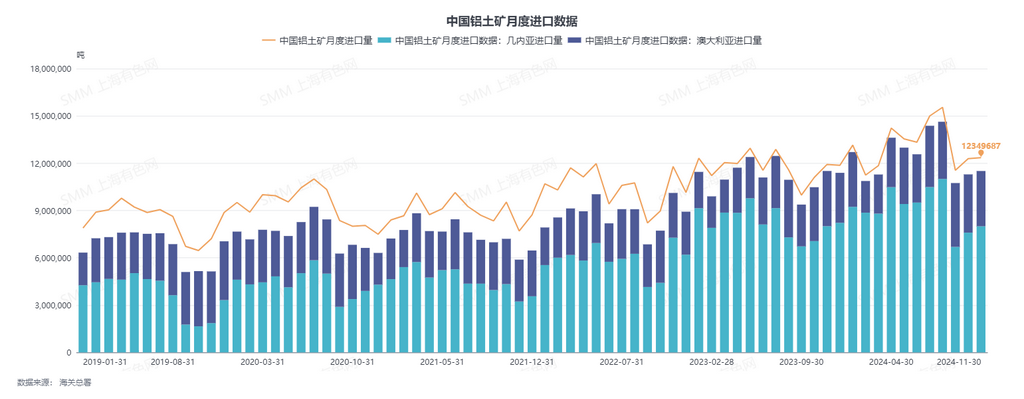

Demand for imported bauxite surged, but supply growth failed to meet demand.

On the demand side for imported bauxite, domestic bauxite supply decreased with no short-term recovery expected. Meanwhile, significant alumina profitability encouraged production increases, prompting some alumina refineries that previously used domestic ore to switch to imported ore to supplement raw material supply, leading to a surge in demand for imported bauxite.

However, disruptions in the supply of Guinean bauxite, the main source of imported bauxite, persisted. From April to May, transshipment disruptions reduced bauxite shipments. From July to September, the rainy season had a greater-than-expected impact, significantly reducing shipments. In October, a Guinean miner suspended exports. These disruptions collectively affected the increase in Guinean bauxite supply. From January to November 2024, China imported a total of 99.919 million mt of bauxite from Guinea, accounting for 69.44% of total imports, up 9.9% YoY.

Although bauxite supply from other sources increased, the overall growth in imported bauxite supply failed to meet the increase in demand, resulting in a significant supply gap for imported bauxite and supporting the continued upward trend in bauxite prices.

The average profit in the alumina industry remains considerable, and underpinned by demand, upward momentum for bauxite prices persists.

Entering Q4, alumina prices surged again, with the average profit in the alumina industry reaching nearly 2,500 yuan/mt. Stimulated by high profitability, alumina enterprises actively increased production, with operating capacity reaching a record high, thereby increasing demand for bauxite and acceptance of high-priced bauxite. Meanwhile, as the rainy season in Guinea ended, bauxite shipments rebounded, bulk transactions became more frequent, and prices for imported Guinean bauxite accelerated upward.

From mid-to-late December to the present, domestic spot alumina prices began to decline. However, as of January 3, 2025, according to SMM's daily cost-profit model for alumina, theoretical alumina profits remained as high as 2,197 yuan/mt. In the short term, alumina refineries are expected to maintain high production enthusiasm. Coupled with the anticipated commissioning of some new domestic alumina projects in Q1 and Q2 2025, there is a demand for stockpiling bauxite raw materials, and short-term bauxite demand is expected to remain high.

On the supply side for bauxite, domestic bauxite production is expected to remain at low levels with no significant short-term increase. For imported bauxite, Guinean bauxite supply is expected to recover, but the onset of the rainy season in Australia may cause a slight pullback in bauxite supply. Overall, the total supply of imported bauxite is expected to see limited short-term growth, and the bauxite market is likely to maintain a supply gap in the short term, with upward momentum for prices persisting.

2025 Outlook: Under a Tight Balance, the Price Center for Bauxite May Shift Higher Compared to 2024

On the supply side, Guinean bauxite is expected to see both capacity expansion and new projects, with an estimated increase of nearly 20 million mt in imported bauxite supply in 2025. Domestic bauxite production is expected to remain low, with a slight recovery in annual production. On the demand side, alumina production in 2025 is expected to increase to approximately 86 million mt, driving higher demand for bauxite. Additionally, new alumina projects are expected to create stockpiling demand for bauxite. Overall, the domestic bauxite market in 2025 is likely to maintain a tight balance, with the annual average price of bauxite expected to rise significantly compared to 2024.

(The above information is based on market data and comprehensive evaluations by the SMM research team. The information provided is for reference only and does not constitute direct investment advice. Clients should make cautious decisions and not substitute this for independent judgment. Any decisions made by clients are unrelated to SMM.)

Data Source: SMM Click here to access the SMM industry database for more information.

(Mingxin Guo, 021-51595800)

![Sellers Show a Strong Willingness to Hold Prices Firm, While Transaction Premiums Continue to Narrow [SMM Spot Aluminum Midday Commentary]](https://imgqn.smm.cn/usercenter/wsCPG20251217171653.jpg)